Well, in the past (and the present in many places) perpetual unrepayable debts were used as a way to implement slavery without calling it slavery. They call it debt peonage. You know, food for thought.

Short term it pads the companies books a bit more by adding an asset on top of the revenue. Medium term it’s a perpetual impairment generator. The executives are just planning to cash out before the inevitable happens.

Because in the summer people run the AC more than they can afford and rack up like $300 bills when their off-summer average would normally be like $70. The loan programs are more like a deferred payment plan where they will cap the individual monthly payment at $150 or something, and then just push the surplus onto other future bills. Then usually when you close the account you owe them a bunch of money still, and that’s when they start doing things like offering to set you up with loan services.

It’s really not. What it does is trap these people in endless debt. Now we don’t know any details about these loans, but there’s no way in hell the customers aren’t going to be paying fees and interest. A loan of $40 will be a loan of $100 the next month and so on. This is a way to make extra off of the people who have nothing.

In the corporate world, if you are taking on debt to fund operations, that’s an indicator that your business is circling the drain. The same applies to personal finance.

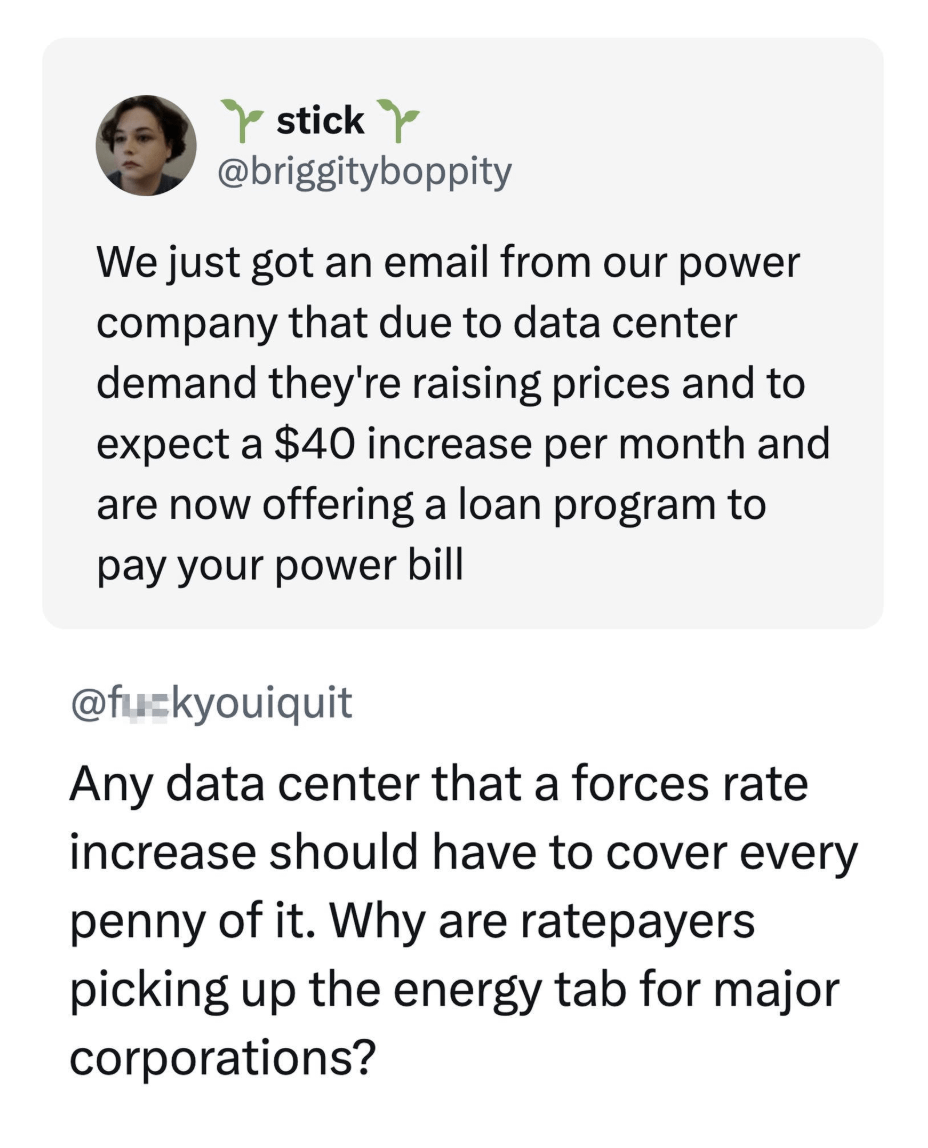

{kind=link}

How the fuck should a loan program help paying for monthly recurring costs?!

Well, in the past (and the present in many places) perpetual unrepayable debts were used as a way to implement slavery without calling it slavery. They call it debt peonage. You know, food for thought.

the more I’m debt you get the more you owe them,

Short term it pads the companies books a bit more by adding an asset on top of the revenue. Medium term it’s a perpetual impairment generator. The executives are just planning to cash out before the inevitable happens.

Because in the summer people run the AC more than they can afford and rack up like $300 bills when their off-summer average would normally be like $70. The loan programs are more like a deferred payment plan where they will cap the individual monthly payment at $150 or something, and then just push the surplus onto other future bills. Then usually when you close the account you owe them a bunch of money still, and that’s when they start doing things like offering to set you up with loan services.

“Capitalism breeds innovation”

Meanwhile we have monthly installments for monthly installments.

I guess they cover you for a while until you figure it out. It’s better than nothing ig.

It’s really not. What it does is trap these people in endless debt. Now we don’t know any details about these loans, but there’s no way in hell the customers aren’t going to be paying fees and interest. A loan of $40 will be a loan of $100 the next month and so on. This is a way to make extra off of the people who have nothing.

That’s more than 1200% interest. Even loan sharks don’t do that.

That example is assuming you’ll accrue another $40 next month. The interest numbers are pulled from my ass to make a point.

In the corporate world, if you are taking on debt to fund operations, that’s an indicator that your business is circling the drain. The same applies to personal finance.

Businesses can afford to go bankrupt. People can’t afford to die. Electricity is a basic necessity for a lot of people.

It helps people who can still pay on average but have an unexpected cost which, due to higher bills, now pushes them into the red.

Have you heard of the concept of company towns?